This isn’t a great business. It isn’t even a good business. But it’s not a terrible one, and that’s what it is being priced as.

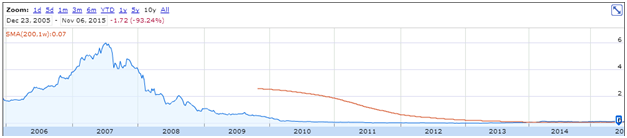

Reverse Corp is in the collect-calling business. It had its heyday, back before the age of mobile phones, but it’s been in steady decline ever since.

During its peak years, it expanded into all sorts of other terrible businesses. It opened new collect calling divisions in European countries and it expanded into payphones. Needless to say, these businesses were crushed after mobile phones came into the picture, and the stock fell from a peak of $6/share to less than a penny per share.

But the board took action. They began a restructuring in 2013 in which they divested all those loss-making divisions. This restructuring, combined with a shift of focus of the company to collect calls from pre-paid cellphones, turned the company around from huge losses to huge profits. They also started a new line of business, an online contact lens store called Ozcontacts.com.

1-800-REVERSE

The idea is, when pre-paid phones run out of minutes, the owner will have to use the company’s service, 1-800-REVERSE, to make a call to anyone. Up until recently, all calls from mobiles cost the user minutes – even calls to 1-800 numbers. However, Reverse Corp was able to negotiate exclusive contracts with the biggest Australian mobile phone companies, Telstra and Vodafone, such that calls to 1-800-Reverse would be the only free call a pre-paid wireless customer could make.

Needless to say, this monopoly on a niche market drove up profit margins. Unfortunately, the Australian government moved to make all 1-800 numbers free from cellphones by the end of 2014. It was expected this would have a huge negative impact on revenues, as the competitors, 1-800-MumDad and 1-800-PhoneHome, would now have access to the pre-paid wireless market, so Reverse Corp shares sold off.

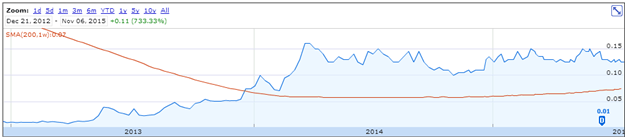

Oddly, the results have been exactly the opposite. In the most recent fiscal year, revenues actually increased 3%, and EBITDA increased by 12%.

Perhaps there is some brand loyalty to 1-800-Reverse, or perhaps pre-paid wireless customers are simply not aware of the change in rules yet. Whatever the reason for this paradoxical increase in revenues, there is evidence that investors should not be discounting the cash flows from this business so heavily.

OzContacts.com

Most of the time, when managers start a new line of business in which they have absolutely no experience, it’s a complete failure. But Ozcontacts has been anything but. Over the course of the last 2 years, the company has grown organically from nothing to a business doing $1.8 million in revenue per year. Over the course of the last fiscal year, it broke even on cash flow, and management reported the business was actually cash flow positive in the last half of FY 2015.

Unfortunately, the business has hit up a wall as far as its growth; revenues are down year-over-year. Management attempted to restructure the business, and states the decrease in revenues is related to a new focus on customer retention and increasing sales per customer rather than increasing the number of customers. It appears the new strategy has at least driven cost improvements:

Management seems to strongly believe in this business. It was started as a JV in which Reverse Corp only owned 65%, however in the last quarter of FY 2015, they bought out their partner, for a current ownership of 95%.

Valuation – Sum of parts

The sum of parts method is probably the best method to value the company; there is a core business that is contributing all of the earnings, another that isn’t, plus a big wad of cash and a hidden tax asset. So first things first – let’s look at cash.

Part 1: Is the Cash worth Cash?

Management plans to use cash on hand to acquire stakes in profitable growing businesses. Normally, this would make me nervous. But the company has a good history of getting in to reasonably good businesses – first with the pre-paid mobile business, and then with the contact lens store. So I think it is most likely they won’t destroy value with any investment.

The cash could be discounted if earnings turn negative on one of the businesses and management doesn’t cut their losses – eating into the big cash pile. But here again, management has a history of divesting loss-making divisions, first with the overseas businesses, and then with the payphone business. If either OzContacts.com.au or 1-800-REVERSE turned unprofitable, I think it’s most likely that management would get rid of it quickly.

Finally, working capital requirements are probably pretty low for these businesses. Since its operations are either run by submitting bills to wireless customers and charging customers online, it doesn’t really need a lot of cash on hand for either of these businesses.

All of this makes me think that the cash is worth near full value, and deserves only a modest discount, if at all. Let’s say 90 cents on the dollar, so $6 million, or $.064 per share.

Part 2: OzContacts.com.au

The business just became profitable, but it is difficult to assess to what degree, because of the inclusion of the unprofitable months at the beginning of FY 2015. Even so, I’d imagine that a profitable online business is worth at least half of sales. It might be worth something more like 1-1.5X sales to a strategic acquirer, like one of the other contact lens stores. So we get to a range from $900,000 in the worst case to $2,700,000 in the best case, or $.01 to $.029, respectively, with a most likely valuation somewhere between that – maybe $.02 per share.

Part 3: 1-800-REVERSE

This is the big question: what is the core collect calling business worth?

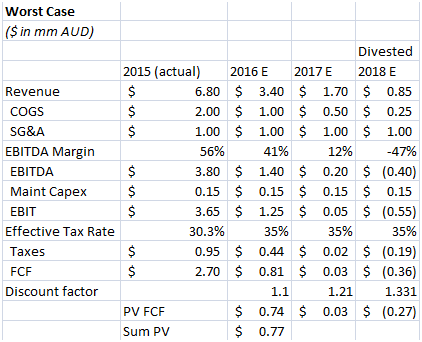

Worst Case:

We could easily say that in the worst case, competition catches up, customers catch on, revenues drop off a cliff, and the company quickly becomes unprofitable and gets divested. In the scenario that revenues drop off by 50% in each of the next two years, 1-800-Reverse would only contribute free cash flow for 2016 and 2017, and become unprofitable in 2018, at which point it would likely be divested. This leads to a valuation for 1-800-Reverse of a little more than $750,000, or $.008 per share.

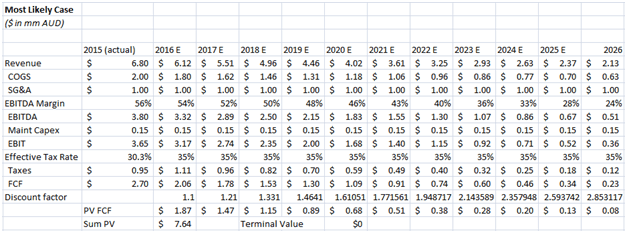

Most-likely:

Considering revenues have actually increased under the new rules, I think it’s likely that the rate of decline in 1-800-REVERSE will be far more modest than 50% per year, maybe something like a 10% decline in revenues per year. Under this assumption, we get to a valuation of $7.6 million, or about $.08 per share.

Best-Case:

Under the best case scenario, we assume flat revenues. Maybe the growth in the population and the market (pre-paid mobile) matches the entry of competition to the market. Maybe the company finds a way to capitalize on a new market (like expanding overseas, except this time, profitably). In either case, it is a possibility that management figures out how to keep up revenues at this pace, with similar kinds of margins. Under this scenario, we get to a valuation of $18.1 million, or $.194 per share – more than the whole company is worth today. (For terminal value, I assumed that after 10 years, the revenue begins to decline at 10% per year).

Part 4: Deferred Tax Assets – a hidden value

The company has about $150,000 in net deferred tax assets sitting on the balance sheet. In addition, they have $750,000 of deferred tax assets sitting off balance sheet in relation to a capital loss. The company can recognize the latter if it realizes a capital gain, if, for example, it sold off OzContacts. If this were to occur, the company could revalue these, and you’d get another cent per share of assets.

Sum of parts

All told, under worst-case-scenario pricing, we get to valuation of $.082 per share – a 34% downside. Keep in mind, this is under extremely aggressive assumptions for decline in 1-800-REVERSE. In the most-likely case, we get to $.164 per share, an upside of 32%. And under the best case scenario? A valuation of $.288, an upside of 130%.

A simplistic valuation check

Things can get hairy quickly doing DCF valuations. But even using a quick multiple check shows us that Reverse Corp is likely undervalued.

The company is trading for 12.5 cents a share and has 93.4 million shares outstanding. We already stated that the value of cash was about $.064 per share. That puts the valuation of the rest of the businesses at 6.1 cents a share, or about 5.7 million.

The company generated $2.8 million in EBIT during fiscal 2015, so that puts the company’s valuation at a measly EV/EBIT of 2 – certainly low enough to merit a deep value investment.

Summary

The company has undergone a turnaround, and even though its core business is undesirable, it is currently throwing off a lot of cash flow. The major determinants of value are

1) Whether 1-800-REVERSE declines in revenues as a result of the 2014 ruling to allow free 1-800 calls from all mobile phones, and whether fewer callers resort to collect calls over time

2) Whether the contact lens business can meaningfully contribute to cash flow or will be put up for sale

3) What businesses the management decides to buy with cash

If you buy the arguments for the best case scenario, then the company offers a pretty good risk/reward of 1 to 3. If not, then at worst it’s a toss-up – about a 1-1 risk/reward. I think it’s entirely possible the company continues to earn at its current rate, and therefore I’ve accumulated a position for myself.