Reverse Corp (ASX: REF) came out with an announcement on the Half-Year ended Dec 31, 2015. I’ve updated my sum-of-parts analysis below.

The Cash

An interesting development in the cash picture has evolved. The company still has net cash of $5.56 million, but has also purchased shares in another Australian company, Onthehouse Holdings, an Australian real estate software company. It initially bought 1.75 million shares at an average price of 57 cents a share, then Onthehouse received a takeout offer. for 75.5 cents a share. The share price rose to 70 cents a share, and Reverse Corp bought another 1.39 million shares, betting the merger would occur. As luck would have it, Onthehouse rejected the initial takeover offer, and the buyers offered to increase the bid to 85 cents a share this morning.

Shares are currently trading at 79.5 cents a share, for a 26% gain from Reverse Corp’s buy-in price. Reverse Corp’s stake now stands at $2.50 million, from an initial investment of $1.98 million. If the deal goes through, the stake will be worth $2.67 million.

That puts cash and marketable securities at $8.06 million, or 8.6 cents per share. For reference, the whole company is trading for 11 cents per share.

Last post, I said the cash probably deserved a 10% discount, as management was looking to make acquisitions, and we have no assurance of the success of these acquisitions. The latest development seems to show that they are at least looking in the right places. I’ll keep the 10% discount, and say cash is $7.25 million or 7.8 cents a share.

OzContacts

OzContacts is positive on EBITDA, but the EBITDA is still miniscule at $35,593. This was probably because of a lower revenue this HY than the previous. It might be consumer weakness in Australia, or it might be weakness in the business. I’m not sure which is the case, and it is worth keeping an eye on. I’ll take my cue if on the next earnings announcement the inventories have built up – that would be a sign that the business has serious problems.

The company wants to make acquisitions in this business, achieve scale, and boost margins through synergies. I would normally say I don’t trust management to be do things like this, but the company has proven itself to be a shrewd capital allocator.

The company divested its loss-making divisions immediately when they stopped contributing to the bottom line, cost-cut their core business to start generating tons of cash flow, started a new business in an area they have no expertise, successfully got the business to profitability, and has been even investing in the stock market with success (more success than I have had lately). Some of these might be luck, but after enough successes in a row, I have to think management must be doing something right.

So I think it’s reasonable that management might succeed at acquiring another contact lens business and cost-cut to realize synergies.

The business is profitable and growing EBITDA (despite the decline in revenues), and probably is still worth at least 1-2 cents a share.

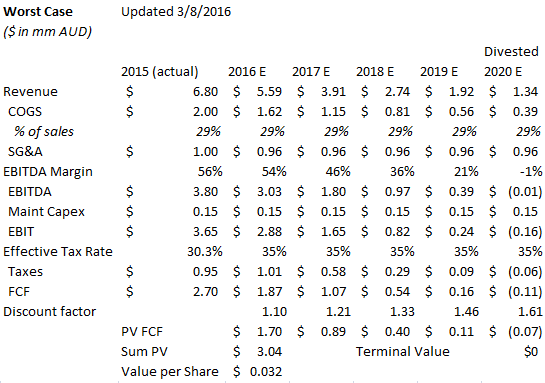

1-800-Reverse

The revenue at Reverse declined 16%, rather than the 50% decline in my worst case, and the 10% decline in my most likely case. So it’s doing a little worse than I thought was likely. I’m now assuming 30% yearly decline in the worst case, a 15% yearly decline in the most-likely, and 5% decline from here on in the best case.

So in the worst case, I won’t lose much (in fact, might even make a little), and in the best case, I might make a lot.

There is room for additional upside. If management deploys capital in an effective way, and is able to realize synergies from a contact lens acquisition, we could see more value in the OzContacts business.

On the 1-800-Reverse side, I think the pre-paid calling business is counter-cyclical and should benefit from the current macro picture. The pre-paid cellphone business grew in the U.S. during the 2009-2010 recession. With Australia in a slump from a decline in the mining sector, and now oil and gas weakness, the pre-paid calling business ought to benefit from tailwinds of a cash-strapped consumer. There is a real possibility that revenues at Reverse Corp actually increase, rather than continue to decline, as consumers shift to pre-paid mobiles.

Finally, the strength of the 1-800-Reverse brand shouldn’t be underestimated. Though there are two competitors in the space, Reverse Corp spent years on advertising to develop recognition among consumers. It can now reap the dividends of those years of investment without need for further advertising. The collect calling industry isn’t big enough to justify large advertising budgets anymore, which essentially locks in the consumer “mind-share” at old 1990’s levels. The competitors can try to buy their way in, but they can’t afford to do the kind of advertising necessary to displace 1-800-Reverse. This mind-share ought to allow keep at least a small moat against the competitors as the industry continues to decline.

Disclosure: I own shares of Reverse Corp